Nov 30

The inflation rate has come down from the forty-year highs we saw in 2022, but it is still elevated. While we are seeing relief on prices, there are some positive impacts of higher inflation.

The IRS sets tax brackets, tax deductions, 401(k), and other tax-efficient retirement savings account contribution amounts by pegging them to inflation. This means you have the opportunity to increase savings for retirement, reduce your tax burden, and earn more without moving into a higher tax bracket. And while inflation will likely continue to decrease, the tax bracket and standard deduction changes and contribution limits are likely to be permanent.

Higher Tax Brackets Can Help You Plan a Multi-Year Strategy

Tax brackets are pegged to inflation to ensure that they reflect real income. Inflation reduces the value of tax credits and exemptions, which means you pay more taxes. Increasing the income range in each tax bracket means more income may be taxed at lower tax rates.

Planning to keep more of your income in the lowest possible brackets can save you considerably on taxes. It requires a multi-year plan to take into account all sources of income and a strategy to take large amounts of taxable income in years in which all income may be lower.

Thinking through sources of income, the tax impacts of larger asset sales, capital gains taxes on investments, and other taxable events can help you devise a multi-year plan. The goal isn’t just to lower taxes in any one year, but instead to lower the amount you pay over the course of your life, whether you are working or retired.

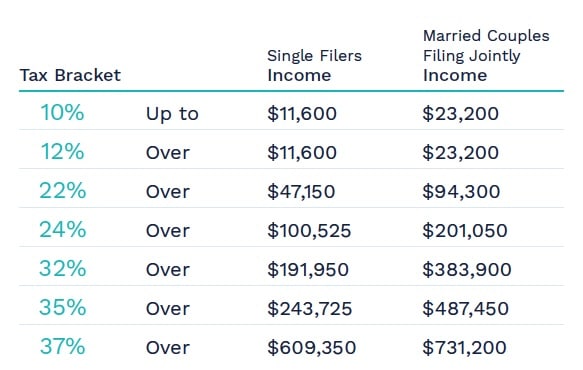

2024 Tax Brackets

The Standard Deduction Increase is Meaningful

The federal standard deduction will increase to $14,600 next year, from $13,850 in 2023, for single files. For married couples filing jointly, the new deduction amount is $29,200. If your mortgage interest, charitable contributions, and the allowable amount of state and local taxes is more than the new standard deduction, it may make sense to itemize. But it’s worth doing the calculation to find out.

You do have an option for charitable gifts that can increase the amount you can deduct. You can “bunch” your charitable gifts that are intended for several years into a single year. This strategy can be effective when all your itemized deductions, including the bunched gifts, are more than the standard deduction.

Retirement and Healthcare Savings Contributions

Retirement savings contributions increased as well. The new maximum contribution limit is $23,000. If you are age 50 or over, you can take advantage of the “catch-up” contribution of $7,500, for a total of $30,500. The new limits don’t just mean increased savings; they also lower your taxable income. The same limits apply to 403(b) plans, many 457 plans, also the Thrift Savings Plan for federal government employees.

IRA limits contribution limits have also increased, to $7,000. The catch-up contribution for an IRA for those age 50+ is an additional $1,000.

Flexible health spending accounts can now accept contributions of up $3,200 of pre-tax dollars to this type of account to pay for medical costs that aren’t covered by insurance.

Health Savings Accounts (HSAs) have new maximum contributions, too. An individual can contribute up to $4,150, and the family contribution has risen to $8,300. The catch-up amount for age 50+ remains the same at $1,000. These accounts are referred to as “triple-tax-advantaged” because you contribute pre-tax dollars that lower your taxable income in the year you contribute, the accounts grow tax-free, and qualified withdrawals are also not taxed.

Social Security Benefits and the Earnings Test Went Up – But So Did Taxes

Social security benefits increased by 3.2%, a more normal increase than the big numbers we’ve seen for the last two years. The maximum monthly benefit for claiming at your full retirement age (FRA) will be $3,822 in 2024. If you’re working while collecting social security, your earnings are subject to an earnings test limit, above which annual benefits are reduced by $1 for every $2 in income over the limit. That limit this year is $22,320.

If you’re still paying into the system, you may be paying a bit more next year. Social security taxes are 6.2% of income, up to a maximum earnings ceiling. The limit increased to $168,600 in 2023. This translates to a dollar amount of $8,400.

The Bottom Line

Taking advantage of the silver lining of inflation by maximizing tax-advantaged savings, and undertaking proactive tax-planning strategies, can help you keep your financial planning on track.

This work is powered by Advisor I/O under the Terms of Service and may be a derivative of the original.

The information contained herein is intended to be used for educational purposes only and is not exhaustive. Diversification and/or any strategy that may be discussed does not guarantee against investment losses but are intended to help manage risk and return. If applicable, historical discussions and/or opinions are not predictive of future events. The content is presented in good faith and has been drawn from sources believed to be reliable. The content is not intended to be legal, tax or financial advice. Please consult a legal, tax or financial professional for information specific to your individual situation.

This content not reviewed by FINRA

White Sand Wealth Management, LLC is an Investment Adviser registered with the State of Missouri. All views, expressions, and opinions included in this communication are subject to change. This communication is not intended as an offer or solicitation to buy, hold or sell any financial instrument or investment advisory services. Any information provided has been obtained from sources considered reliable, but we do not guarantee the accuracy or the completeness of any description of securities, markets or developments mentioned. We may, from time to time, have a position in the securities mentioned and may execute transactions that may not be consistent with this communication’s conclusions. Please contact us at 816-429-6743 or Joel@wswm.net if there is any change in your financial situation, needs, goals or objectives, or if you wish to initiate any restrictions on the management of the account or modify existing restrictions. Additionally, we recommend you compare any account reports from White Sand Wealth Management with the account statements from your Custodian. Please notify us if you do not receive statements from your Custodian on at least a quarterly basis. Our current disclosure brochure, Form ADV Part 2, is available for your review upon request. This disclosure brochure, or a summary of material changes made, is also provided to our clients on an annual basis.

Stay In Touch