Shocks at Home and Abroad

The market barely had time to digest tariffs and AI when the Trump administration began a war against Iran. After the initial reaction, the market appeared to recover somewhat, as investors likely began to lean towards the conflict not being drawn out over a longer time horizon.

Oil prices have increased precipitously, and recent guidance from the White House has been that winning the war is more important than rising oil prices. However, the administration is also continuing to pull all available levers to cushion the shock.

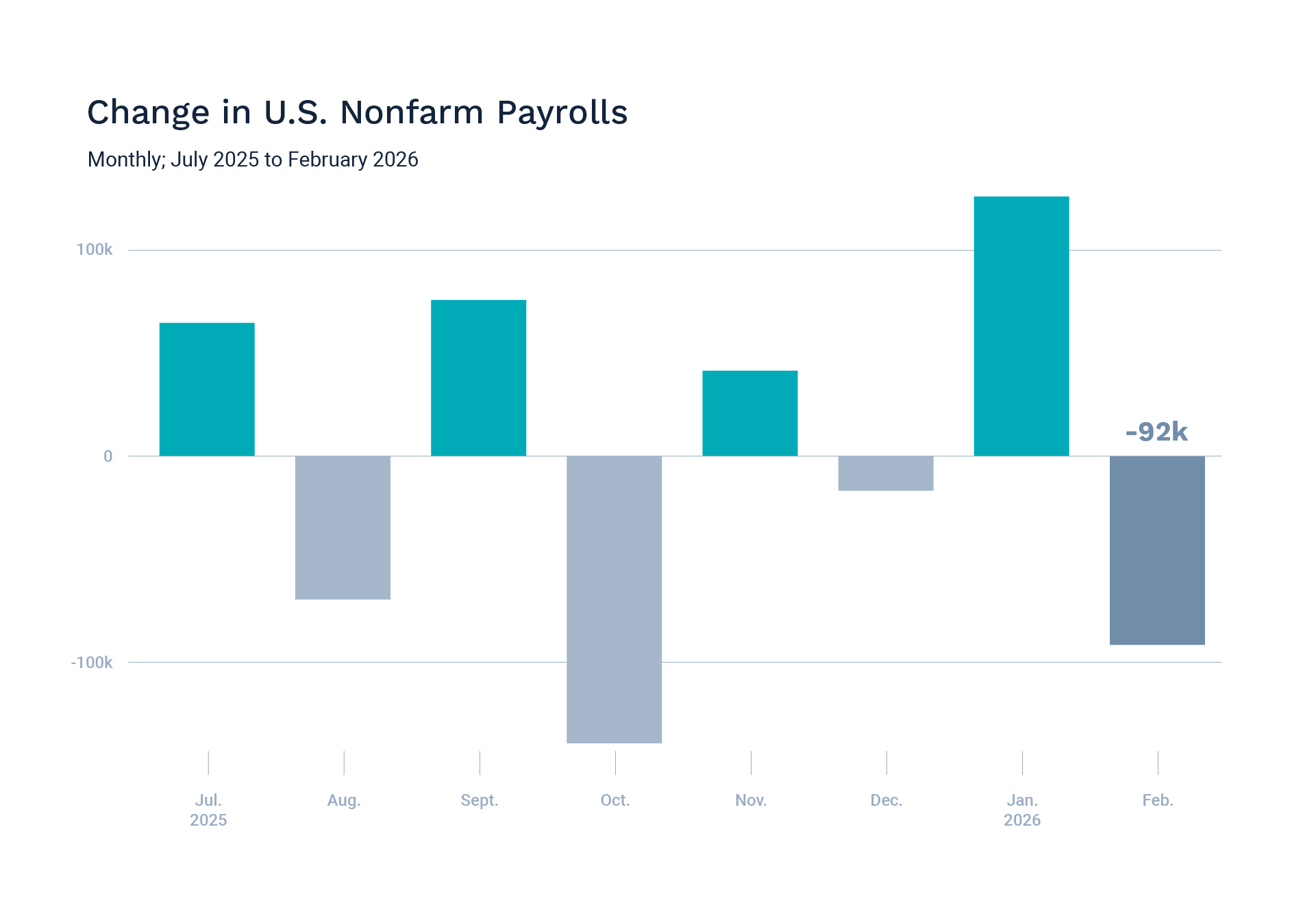

On the domestic front, the labor market surprise was a loss of 92,000 jobs, and a downward revision of the previously reported January numbers. This would seem to indicate a labor market that isn’t easily throwing off AI disruption, tariff uncertainty and ongoing immigration crackdowns.

Where do we stand at the Ides of March? A slowing economy, a struggling labor market, and the added risk of a war that could strangle the movement of oil and drive up prices – and inflation.

Let’s get into the data:

- Non-farm payrolls for February fell by 92,000. The U.S. Bureau of Labor Statistics reported that the labor market fell by 92,000, compared to the increase of 50,000 jobs that were expected, and the unemployment rate rose to 4.4%.

- Inflation remained unchanged. The Bureau of Labor Statistics reported that the Consumer Price Index for February grew 2.4% from twelve months ago.

- The University of Michigan Consumer Sentiment Index fell. The index read 55.5 in early March, down 1.9% from the previous month.

- Real GDP revised down. The first revision of GDP saw the previous estimate of 1.4% for the fourth quarter cut in half, to 0.7%.

What Does the Data Add Up To?

It’s not all gloom and doom. The Business Roundtable CEO Economic Outlook Index rebounded in the first quarter as companies planned to increase capital spending, largely around AI. Unlike normal cycles when rising sales and increased capital expenditures lead to hiring, the AI focus makes that a little more uncertain.

The consumer is reacting by keeping spending steady at 0.1% in January, but the savings rate bumped up half a percentage point to 4.5%, a sign that consumers are a becoming more cautious about the future.

The big question is around the upcoming actions of the Federal Reserve. The pressure for rate cuts from the administration has been clear, and the current nominee for Fed Chairman, Kevin Warsh, appears poised to want to deliver them. With prices already high and a potentially longer-term increase to gas prices, as well as other prices that will increase as disruption from the Iran war grows, inflation or stagflation becomes a very real risk to the economy.

Chart of the Month: Labor Turns to the Negative

Looking at the stark reality of the numbers shows a labor market that is struggling at best, as strong performance one month gets revised down the following month, and the market turns negative.

Source: Bureau of Labor Statistics; Axios Visuals

Equity Markets in February

- The S&P 500 was down 0.9% in February

The stocks hit the worst included software and insurance stocks, as investors reacted to the potential for AI disruption in these industries. By the end of the month, headlines had turned somewhat as market observers began to feel that perhaps the sell-off had been overdone. The surprise in the market was non-response to the U.S. Supreme Court’s February 20th ruling against broad tariffs. The index rose only slightly from the ruling through the end of the month.

Utilities were the biggest gainer in February, with a 9.9% increase, followed by Energy, up 8.8%. Consumer Discretionary was the sector most in the red, with a 5.4% decline.

Bond Markets in February

The 10-year U.S. Treasury ended the month at a yield of 4.21%, down from 4.24% the prior month. The 30-year U.S. Treasury ended February at 4.64%, down from 4.84%. The Bloomberg U.S. Aggregate Bond Index returned 1.64% in February. The Bloomberg Municipal Bond Index returned 1.25% for the month.

The Smart Investor

It can be difficult to remain focused on your goals when faced with relentless headlines that all seem to identify some new threat.

Trying to select data and make sense of a developing theme or trend can often result in more confusion and even paralysis. The way to manage through extreme volatility is to fall back on the plans you made before volatility hit. Your long-term investment plan should be crafted to take into account market swings and economic downturns. So far, nothing material has happened.

As we close in on the end of tax season, focus instead on your goals and plans for the upcoming year. With extreme market volatility, dollar-cost averaging investments makes more sense. If you plan to invest your tax refund, set up a plan to invest it over time to minimize the impact of daily market shocks.

We’re always here to answer your questions, and help you navigate over the bumps!

This work is powered by Advisor I/O under the Terms of Service and may be a derivative of the original.

The information contained herein is intended to be used for educational purposes only and is not exhaustive. Diversification and/or any strategy that may be discussed does not guarantee against investment losses but are intended to help manage risk and return. If applicable, historical discussions and/or opinions are not predictive of future events. The content is presented in good faith and has been drawn from sources believed to be reliable. The content is not intended to be legal, tax or financial advice. Please consult a legal, tax or financial professional for information specific to your individual situation.

This content not reviewed by FINRA

Stay In Touch