We’re a little more than a month into the war with Iran, and recent data releases are beginning to tell a story of the impact on the economy. Growth expectations are lower, inflation is higher and consumer sentiment is tanking.

The bond and equity markets have been reacting to the headlines, but there is beginning to be a feeling that the markets may already be pricing in ongoing anxiety and uncertainty about Iran. While anything can happen, the breakdown of talks over the weekend does not seem to have rattled investors. This may be an echo of the reaction last year to tariffs. Once the shock of Liberation Day wore off and the ups and downs of the ongoing tariff wars became a backdrop, markets recovered.

One key element of market performance last year was that in the long term, the feared devastation of tariffs on the economy did not materialize. While there are certainly significant threats to the economy from the energy shock resulting from the Iran war, there are also scenarios in which they are short-lived, and the economy remains on a solid footing.

Let’s get into the data:

- Non-farm payrolls for March rose by 178,000. The U.S. Bureau of Labor Statistics reported that the labor market rose by 119,000 more jobs than the Dow Jones consensus estimate, after falling precipitously by a revised 133,000 jobs last month. The unemployment rate fell to 4.3%, from 4.4% last month.

- Inflation spiked. The Bureau of Labor Statistics reported that the Consumer Price Index for March grew 3.3% from twelve months ago. The month-over-month number was 0.9%, clearly indicating that the spike was related to the war in Iran.

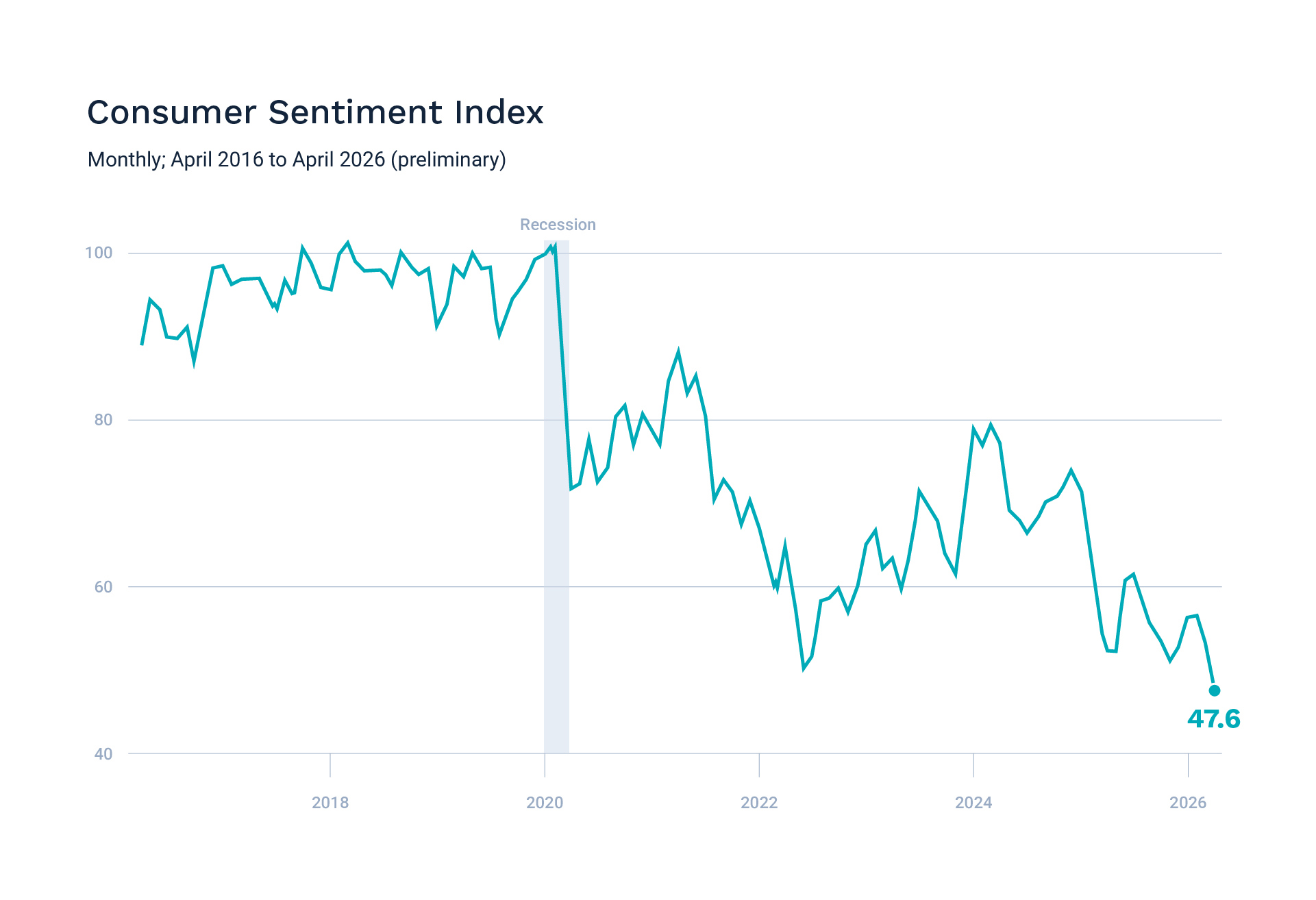

- The University of Michigan Consumer Sentiment Index fell off a cliff. The preliminary reading for April was down 11%, to 47.6. If the full data reflects the same sentiment, it will be the lowest reading on record.

- GDP expectations revised down. The latest GDPNow estimate from the Atlanta Fed is for growth of 1.3% in Q1.

What Does the Data Add Up To?

The markets appear to be taking a long view of the Iran conflict situation, with hopes that the positive market sentiment that we are seeing is not just a relief rally but instead has legs.

Consumers are a lot more pessimistic. Consumer expectations over the next twelve months, as tracked by the Michigan Consumer Expectations Survey, are for 4.8% inflation, up from 3.8% in March. Even more concerning, expectations for longer term inflation also ticked up, to 3.4% from 3.2%. Longer term views for higher inflation are a problem for the Fed, because expecting higher inflation tends to be a self-fulfilling prophecy. Consumers modify their spending by shifting it to the near term, which pushes prices up.

The Fed held rates steady at the March FOMC meeting, and a recent statement from Chicago Federal Reserve President Austan Goolsbee cited the possibility that high oil prices resulting from the Iran war could push rate cuts to 2027.

This would clearly be at odds with the frequently stated desire of the Trump administration for lower rates, but even if Kevin Warsh is confirmed on schedule, the backdrop of spiking inflation may make it difficult to jump start rate cuts at the summer meetings in either June or July.

The other interest rate that has an impact on the economy is the mortgage rate, and it’s going in the wrong direction. Mortgage rates had finally been trending down in 2026 but have increased almost half a percentage point in recent weeks. Existing home sales are now below the 2025 pace, according to the National Association of Realtors. Home loan applications have now fallen for four consecutive weeks.

The longer the Iran war goes on, the higher the likelihood that the current energy shock becomes an energy crisis. Even if a negotiated end to the conflict is reached soon, getting shipping back to normal isn’t as easy as flicking a switch. There will likely be delays even as things normalize.

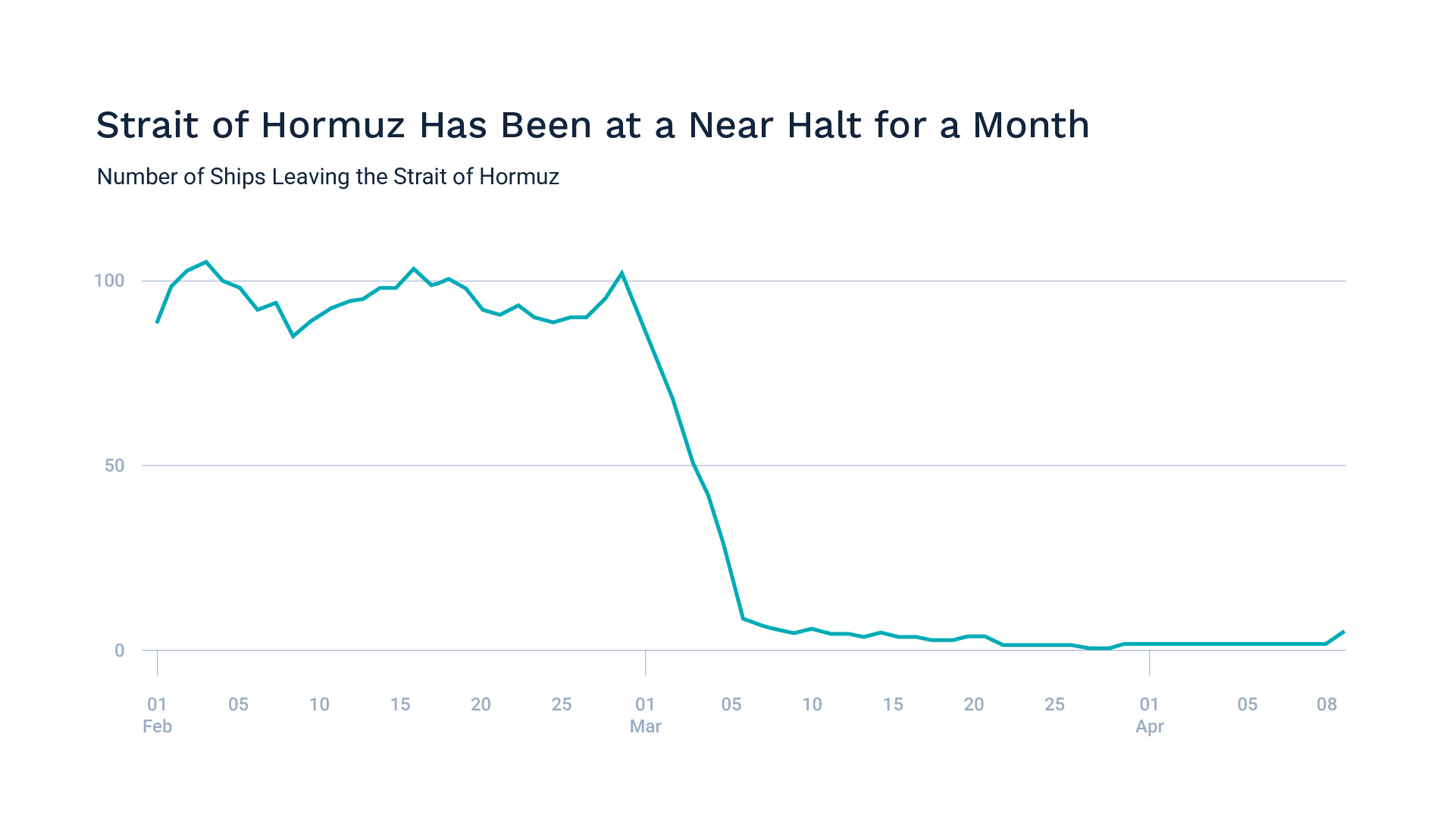

Charts of the Month: Energy Shock and Consumer Sentiment

This month needed two charts to capture what’s going on.

First up, the precipitous decline in tanker traffic has clearly begun to hit the economy. While the market appears to be holding up, if the energy shock continues, the economy will begin to suffer across multiple dimensions.

Source: Bloomberg

Next up, consumer sentiment has fallen over a similar cliff. The 11% drop reflects a pessimistic outlook on the economy, most likely driven by the conflict with Iran.

Source: Axios

Equity Markets in March

The S&P 500 was down 5.0% in March, pushing the year-to-date performance into the red. March saw high volatility that ended with the index down, with ten of the eleven sectors turning negative, led by industrials and technology.

By mid-April, the market had recovered all of March’s underperformance and was flat for the year, tracing a deep V-shape of decline and recovery.

Bond Markets in March

The 10-year U.S. Treasury ended the month at a yield of 4.30%, up from 4.21% the prior month. The 30-year U.S. Treasury ended February at 4.88%, up from 4.64%. The Bloomberg U.S. Aggregate Bond Index fell by 1.76% in March. The Bloomberg Municipal Bond Index declined by 2.32% for the month.

The Smart Investor

The first quarter of the year has been marked by worry, uncertainty and crisis on multiple fronts. Relief on tariffs was accompanied by headlines over growing worries about the disruptive potential of AI, and before those faded away, a war, an energy shock, a steep bump in inflation and wildly swinging labor statistics refocused everyone on the perception of a precarious economy.

But is it really so precarious? Unemployment remains low. Inflation was driven higher by energy prices, but core inflation, which strips out that volatile category, is still healthy.

There are two areas to think about when confronting worry about finances: your investment plan and your budget. In both cases, breaking them down into long-term and short-term can help.

Your long-term strategic investment plan should be built to take into account your risk tolerance and your goals, so you can hit your milestones and still sleep at night. In the short term, your “tactical” investment plan can be tweaked to provide extra risk mitigation, or to seek opportunity in short-term dislocations.

Your long-term budget is how you ensure you make good financial decisions, stay on top of expenses, and meet your savings goals. In the short term, looking at expenses with a critical eye and prioritizing what is important can help you get over rough patches when prices are higher.

With tax season over, spring is the perfect time to tune up your investing and budgeting, so you can sail into vacation season in great shape.

We’re always here to answer your questions, and help you navigate over the bumps!

This work is powered by Advisor I/O under the Terms of Service and may be a derivative of the original.

The information contained herein is intended to be used for educational purposes only and is not exhaustive. Diversification and/or any strategy that may be discussed does not guarantee against investment losses but are intended to help manage risk and return. If applicable, historical discussions and/or opinions are not predictive of future events. The content is presented in good faith and has been drawn from sources believed to be reliable. The content is not intended to be legal, tax or financial advice. Please consult a legal, tax or financial professional for information specific to your individual situation.

This content not reviewed by FINRA

Stay In Touch