The ongoing war with Iran appears to have no clear off ramp in sight, and the ceasefire seems to be on tenuous ground.

The equity markets, responding in part to a historically strong earnings season, have been hitting new highs, even if only temporarily. The bond markets are more pessimistic. The about-face in expectations for the path of interest rates, driven by spiking inflation, has caused yields to be volatile and rise steeply.

The data is reflecting the uncertainty. Consumer expectations are at very pessimistic levels, but consumer spending keeps rising, even as consumers have to dip into their savings. Labor markets are described as “stabilizing,” which apparently means two months in a row of positive numbers. Headline CPI is rising quickly, driven by the fuel shock, but expectations are rising that it will begin to bleed over into other areas.

How is the Federal Reserve going to react? Chairman Powell finishes his term on May 15, and the new Chairman will likely be confirmed with by a very narrow majority, signaling lack of bi-partisan support.

Let’s get into the data:

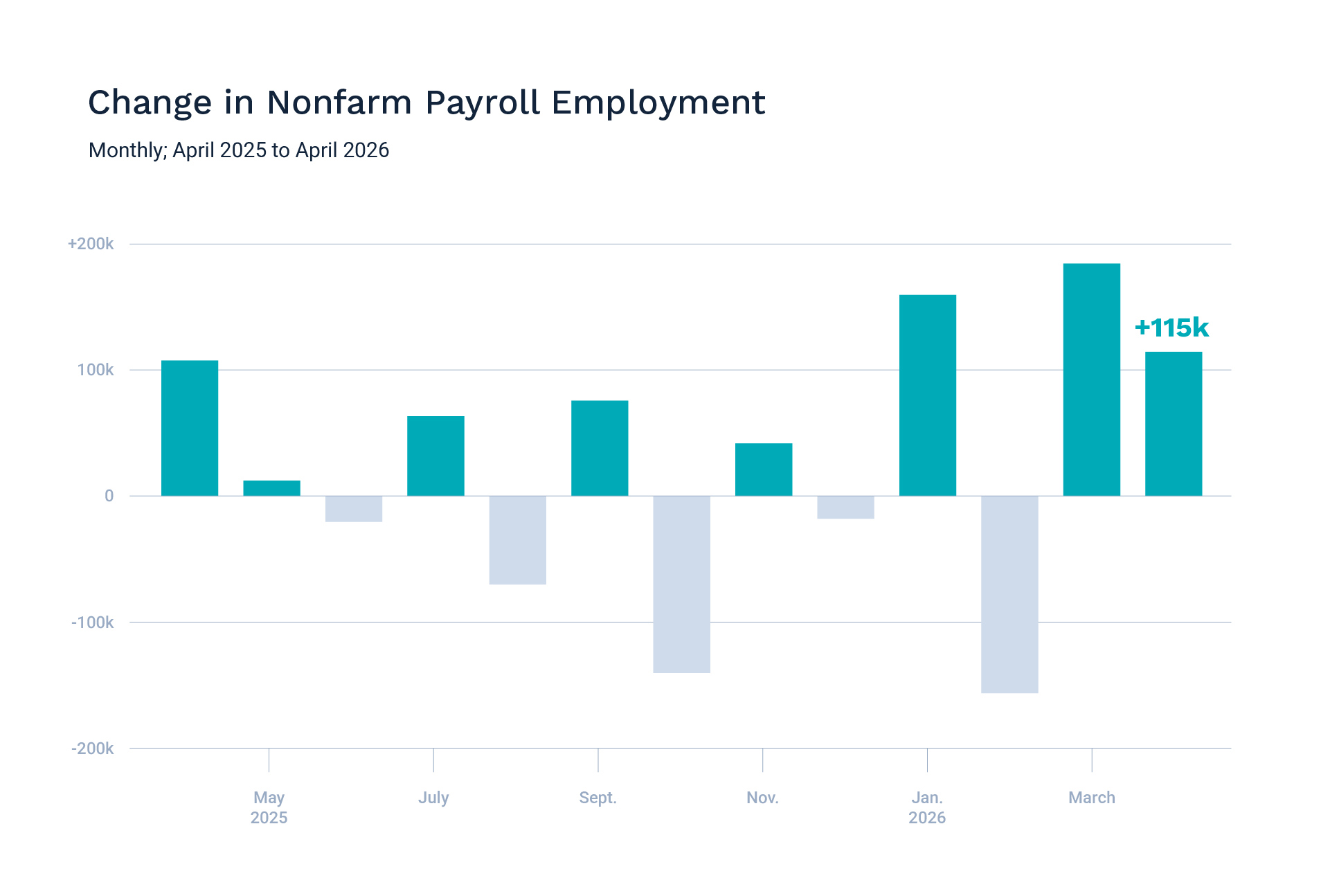

- Non-farm payrolls for April rose by 115,000. The U.S. Bureau of Labor Statistics reported that the labor market rose by almost double the 62,000 jobs of the Dow Jones consensus estimate. This marks two months of job gains, breaking the see-saw trend of gains and losses.

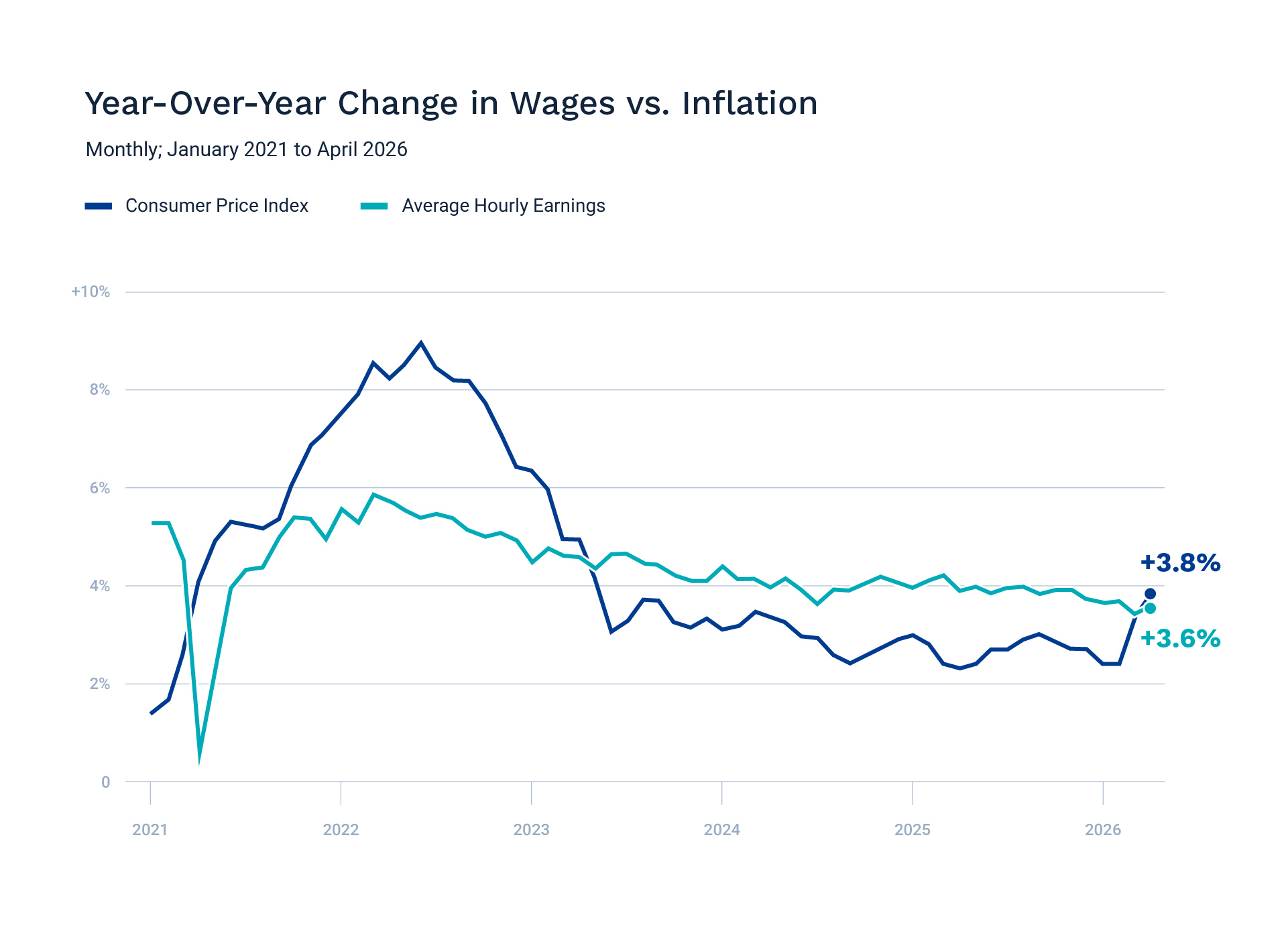

- Inflation on the rise. The Bureau of Labor Statistics reported that the Consumer Price Index for April grew 3.8% from twelve months ago, the highest level we’ve seen since 2023. The month-over-month number was 0.6%, moderating a little from last month at 0.9%.

- Consumers are still spending. The latest CNBC/NRF Retail Monitor, released by the National Retail Federation, showed that retail sales rose for the seventh straight month in April, coming in at 5.73% year over year.

- GDP expectations bounce back. The latest GDPNow estimate from the Atlanta Fed is for growth of 3.7% in Q2.

What Does the Data Add Up To?

GDP expectations have bounced back, and consumers are still spending. The problem is that they are dipping into savings to do it. The personal savings rate was 3.6% in March, marking the lowest rate since 2022. Retail CEOs are sounding the alarm, particularly for consumers in lower-income brackets, that high gas prices and consistently rising inflation will begin to impact consumer behavior.

Another wrinkle is the labor market, where the monthly non-farm payroll number has been strong for two consecutive months, but the steep rise in inflation has resulted in wage growth not quite meeting the rise of the cost of living, as expressed by CPI.

Expectations for the path of interest rates are that we likely will not see rates fall again until 2027, largely due to the upward trajectory of inflation.

After completely misjudging the serious and long-term nature of the rampant inflation the economy experienced after COVID, the Federal Reserve has spent the last several years working diligently to get inflation to a level that is consistently at the target rate of 2% over the long term. With some very similar shocks to the system happening now, in the form of tariffs and ongoing war that is choking off supply of energy, are we in for another long period of rising inflation?

As of now, the Federal Reserve doesn’t appear to think so. The president of the San Francisco Federal Reserve, Mary Daly, looks at a diagnostic tool that tracks multiple inflation indicators against historical norms, and flashes a warning. The tool is showing core goods and import prices are not shading into deep red as of yet. Energy is more concerning, as the longer the situation at the Strait of Hormuz goes on, the more potential it has to affect downstream supply chains.

All eyes will be on the new Federal Reserve Chairman, Kevin Warsh, at the next FOMC meeting in June. While rates are largely expected to remain the same, the first press conference by the Chairman will be very eagerly awaited, as he sets the tone for how he will communicate the Fed’s goals and decision-making process.

Charts of the Month: Labor Markets and Inflation vs Wages

Two charts this month to capture the breadth of the economic data.

While one swallow does not a summer make, two months of positive non-farm payrolls appears to signal a stabilizing labor market.

Source: Axios/Bureau of Labor Statistics

The problem is that while jobs are stable, wage growth isn’t keeping up with inflation that is rising steeply.

Source: Axios/Bureau of Labor Statistics

Equity Markets in April

The S&P 500 was up 10.49% in April, as the market recovered earlier losses despite an ongoing backdrop of uncertainty. Technology shrugged of fears of “AI Armageddon,” with the sector rising almost 20%. There was a preference for growth over value, with growth stocks up 12.4% and value stocks rising 7.2%.

It has been a historically positive earnings season. As of early May, 84% of S&P 500 companies exceeded earnings estimates, beating the five-year average of 78%, according to FactSet.

Bond Markets in March

The 10-year U.S. Treasury ended the month at a yield of 4.39%, up from 4.30% the prior month. The 30-year U.S. Treasury ended April at 4.98%, up from 4.88%. The Bloomberg U.S. Aggregate Bond Index scraped a positive return of 0.39%. The Bloomberg Municipal Bond Index rose by 1.15% for the month.

The Smart Investor

As we head into the summer season, we are higher gas prices, overall higher inflation, and likely no relief on interest rates.

Investors that want to enjoy the summer season to the fullest, but also keep their financial plans on track, should think about cash flow planning and risk tolerance.

Cash flow planning is different than budgeting. Budgets are for your day-to-day expenses. Cash flow planning is more strategic and long-term, taking into account all of your inflows and outflows, and then engaging in big-picture thinking to direct cash to strategic goals, whether that means paying off debt or increasing savings, for example.

With equity markets up, it’s tempting to let things ride. However, given the volatility of the markets this year and the outsized returns in certain sectors, you may want to look at your investments and make sure your risk targets are still intact.

Summer will be here, and then gone, before we know it. Getting your finances in shape before it kicks off can help you enjoy the lazy, hazy days.

We’re always here to answer your questions, and help you navigate over the bumps!

This work is powered by Advisor I/O under the Terms of Service and may be a derivative of the original.

The information contained herein is intended to be used for educational purposes only and is not exhaustive. Diversification and/or any strategy that may be discussed does not guarantee against investment losses but are intended to help manage risk and return. If applicable, historical discussions and/or opinions are not predictive of future events. The content is presented in good faith and has been drawn from sources believed to be reliable. The content is not intended to be legal, tax or financial advice. Please consult a legal, tax or financial professional for information specific to your individual situation.

This content not reviewed by FINRA

Stay In Touch